- Blog

- Contact Client login

650 NE Holladay Street,

The Liberty Centre, Suite 1500

Portland, OR 97232

Skewed to the Top: How passive investing may be affecting pricing

By Bryan Shipley, CFA, CAIA

Passive investment management: A passively managed fund seeks to match the performance of an index by replicating the index’s holdings. Passive investment management delivers market returns, and typically has lower fees than active management.

Over the past decade, investor preference for passive investing has dramatically altered equity markets. This huge movement toward index investments (inflows to passive investments of more than $200 billion annually in 2016 and 2017) may have repercussions on equities’ pricing and valuation, the implications of which should be considered by investors. While we understand there are valid reasons many investors have shifted their preference to more index-based solutions, it would also be naïve not to be aware of the unintended consequences of this shift.

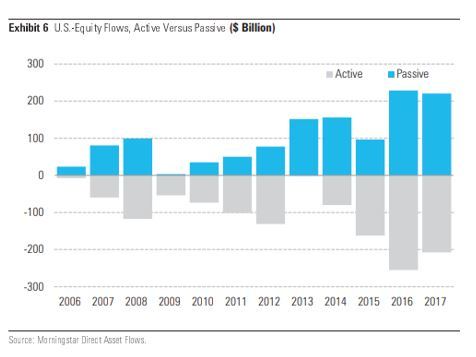

U.S. Equity Flows, Active Versus Passive: Passive strategies have been gaining inflows ($ billions)

Passive investing can play a very important role in portfolio construction by systematically capturing market returns while reducing investment costs, but it is indiscriminate in regard to what an investor pays for ownership in an underlying business. Active management has historically played a key role in pricing assets, as active managers and investors evaluate the current and future prospects of each stock to determine an appropriate market consensus value. Passive investing has relied on this price discovery effort to establish reasonable valuations for stocks, but there are signs the shift to passive investing may now be driving stock prices, a situation reminiscent of the tech bubble of 1998-99, which was the last time we saw disproportionate flows to passive investments.

The basic formula for passive strategies is that each investor owns every underlying holding in the index based on its current weight and price, regardless of its fundamentals (growth, quality, balance sheet, or business prospects). In a hypothetical market consisting entirely of passive investments, if the market were to rise by 10%, each stock’s price would also rise 10% respectively (as represented by the 100% Index in the table below). In other words, stock prices would be a function of their weight in the index, not their fundamental qualities. Clearly, markets aren’t entirely passive as in this hypothetical model, but estimates suggest that approximately 60% of the U.S. stock market is now in passive or quantitative-based investment vehicles. As the chart below indicates, flows to index funds have dominated over those directed toward actively managed funds. It’s unclear just how much this has impacted pricing but is potentially concerning.

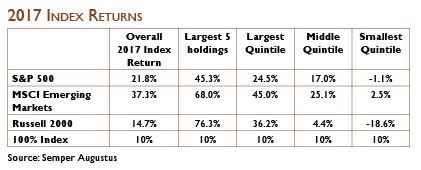

In 2017, a very unusual pattern developed in which the largest companies in each index disproportionately outperformed smaller companies, which was likely driven by the shift from active to passive strategies. Small cap stocks, as measured by the Russell 2000 Index, saw nearly a 100% spread in market returns between the largest five holdings and the smallest quintile, which is nothing short of astonishing. Historically, market returns have been much more homogenous and broadly distributed. In the table below, you can see the nearly perfect stair-step returns of 2017 in several indexes.

While the table highlights only a handful of indexes, the phenomenon was largely consistent across all market capitalizations, regions, and styles in 2017. The most reasonable conclusion from these results is that capital flows directed primarily toward passive strategies created an environment in which the largest index holdings experienced the largest gains primarily driven by their weight in the index, while the smallest suffered due to selling pressure on these stocks. Imagine feeding your chickens based only on their size; the large would grow increasingly larger, and the smaller would not survive.

Index investing tends to perform well in longer duration market expansions and periods that favor growth over value. The winners gain a larger share of the pie, and as long as the music continues to play, this dynamic perpetuates itself. 2017 marked the ninth year of a market that generally fit this pattern.

The last time we saw this kind of euphoric behavior and indiscriminate buying from passive investors was in 1999. At that time, the largest companies included Microsoft, GE, IBM, Wal-Mart, and Cisco It’s important for investors to note that over the following 18 years, each of these companies (aside from Wal-Mart) substantially underperformed the broad S&P 500. Microsoft and Exxon Mobile are the only remaining top ten S&P 500 companies from 1999 that have retained that top ten title; all of the others were replaced by today’s generation of winners, such as Facebook, Amazon, Apple, and Alphabet (aka Google). In other words, the passive approach did not identify long-term winners.

This trend toward passive investing shows no sign of slowing down, and we’ll likely continue to recommend client portfolios that incorporate both active and passive investment strategies, with a tilt toward active specifically because of this issue. But we are paying attention to the possible unintended consequences stemming from this massive movement toward passive investing, and to the opportunities that may present themselves to investors who are willing to objectively challenge the pros and cons of both active and passive investing.

The reality is that the investment world needs active management to aid in price discovery. When we enter an environment in which a market dominated by passive strategies — as opposed to fundamental research — is determining company valuations, as in the last few years, it should cause some concern. In this age of automation, machine learning, and quantitative approaches, it is easy for investors to forget the underlying rationale for owning stocks. These aren’t just pieces of paper or electrons floating around; they represent actual ownership of an underlying business and the economic prospects of that holding in the real economy.